Every salaried professional in India is familiar with the profound sting of payday realization—the stark, undeniable discrepancy between the impressive Cost to Company (CTC) promised in an offer letter and the actual, tangible cash credited to the bank account. For decades, the Indian payroll system has been a labyrinth of creative allowances, structured primarily to maximize monthly cash flow while minimizing statutory social security contributions. Employers routinely pegged Basic Pay at a meager 20% to 30% of the total CTC, padding the rest with a dizzying array of reimbursements, special allowances, and flexible benefit plans.

However, the landscape of Indian payroll and personal finance is undergoing a seismic shift. The implementation of the new labor codes—specifically the Code on Wages—coupled with the monumental transition to the brand-new Income Tax Act 2025 (effective April 1, 2026), has fundamentally rewritten the rules of salary structuring. As a certified Indian Chartered Accountant and HR consultant, I am here to tell you that these changes will impact every single salaried employee across the nation.

Whether you are an entry-level executive or a C-suite veteran, your take-home salary is going to change. For many, the monthly cash-in-hand will drop, while long-term retirement savings will swell. Understanding this complex new reality is no longer optional; it is a financial necessity.

In this comprehensive, authoritative guide, we will decode the critical 2026 take-home salary rules, deep-dive into the mandatory 50% Basic Pay Rule, explore the domino effect on your Provident Fund (PF) and Gratuity, and navigate the updated tax slabs introduced in the Income Tax Act 2025.

How to Use the 2026 Salary Calculator

To eliminate the guesswork from your financial planning, we have developed a state-of-the-art interactive 2026 Take-Home Salary Calculator (located right above). Before you dive into the deep financial mechanics outlined in the rest of this article, here is a step-by-step guide to calculating your exact net pay under the new 2026 regulations:

- Enter Your Total CTC: Input your gross annual Cost to Company (e.g., ₹15,00,000). Ensure this figure includes all components, including employer contributions to PF and Gratuity.

- Set the Basic Pay Percentage: By default, our calculator locks this at 50% to comply with the 2026 Code on Wages mandate. However, if your employer sets a higher basic salary (e.g., 60%), you can adjust this slider accordingly.

- Choose Your City Type: Select “Metro” or “Non-Metro.” This is critical for accurate House Rent Allowance (HRA) calculations if you are opting for the Old Tax Regime.

- Input Section 80C and Other Deductions: If you are claiming deductions (e.g., Life Insurance, PPF, ELSS, Home Loan Interest), enter these amounts. Note: This will only be applied if you select the Old Tax Regime.

- Select the Tax Regime (Old vs. New): Toggle between the outgoing framework and the new Income Tax Act 2025 framework to see a side-by-side comparison of your monthly take-home pay and annual tax liability.

Once you hit “Calculate,” the tool will instantly run hundreds of background payroll algorithms to present your accurate Gross Salary, Net Taxable Income, Statutory Deductions, and Final In-Hand Cash.

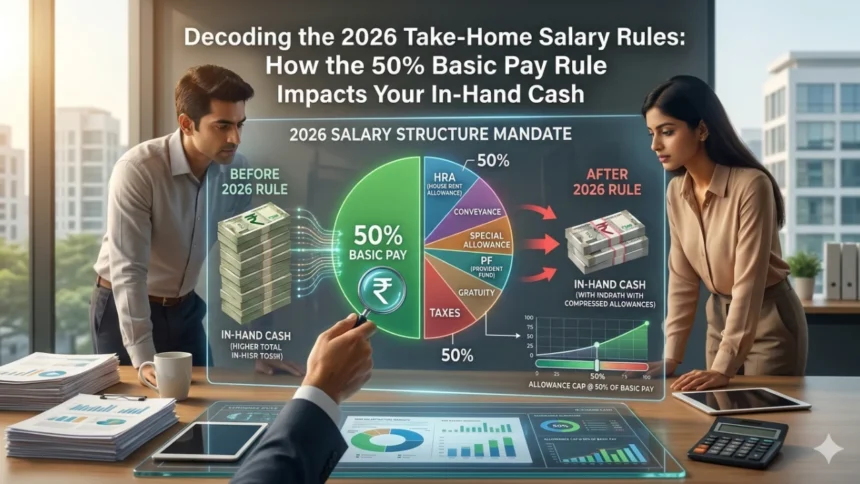

The 50% Basic Pay Mandate Explained

For years, HR departments across India operated on a simple heuristic: keep Basic Pay as low as legally permissible to reduce the burden of statutory contributions like Employee Provident Fund (EPF) and Gratuity, thereby giving the employee a higher take-home salary and reducing the employer’s overall cost burden. A typical ₹10 Lakh CTC might have featured a mere ₹2.5 Lakh Basic Pay.

Those days are officially over.

Under the sweeping reforms of the new labor laws, the government has mandated a strict definition of what constitutes “Wages.” The most disruptive element of this definition is the 50% Basic Salary Rule.

What is the 50% Rule?

According to the new regulations, an employee’s Basic Pay (which includes Basic Salary, Dearness Allowance, and Retaining Allowance, if any) must strictly constitute at least 50% of the employee’s total gross salary.

If an employer attempts to structure a CTC where allowances (such as HRA, Special Allowance, Leave Travel Allowance, Books and Periodicals Allowance) exceed 50% of the total compensation, the excess amount will automatically be deemed as “Basic Wages.” This means the payroll system will forcefully calculate statutory deductions on that excess amount.

Why Did the Government Enforce This?

From the viewpoint of the government and the Supreme Court of India, the previous model of highly allowance-heavy CTC structures was detrimental to the long-term financial security of the Indian workforce. Allowances are, by nature, variable and often tied to specific expenses. Basic Pay is the foundational rock of a salary, dictating the accumulation of retirement corpuses. By keeping basic pay artificially low, employers were inadvertently (or intentionally) stunting the growth of employees’ EPF and Gratuity balances.

Capping allowances at 50% forces companies to create a transparent, robust salary structure. It guarantees that a massive portion of the Indian salaried class will retire with a significantly larger safety net, immune from the temptations of short-term, discretionary spending.

More Read

The Domino Effect on PF and Gratuity

The 50% Basic Pay rule is not just a cosmetic change in HR nomenclature; it triggers an immediate and powerful domino effect across all statutory calculations. When you artificially raise the floor of the Basic Salary, everything tethered to it rises in tandem.

The Mathematics of Provident Fund (PF) in 2026

Under the Employees’ Provident Funds and Miscellaneous Provisions Act, the standard PF contribution is set at 12% of the Basic Salary (with the employer matching this 12%, subject to certain wage ceilings).

Let us look at how the forced restructuring impacts your deductions:

Scenario: A total CTC of ₹12,00,000 per annum.

- Under the Pre-2026 Structure:

- Basic Pay (set at 30%): ₹3,60,000 per year (₹30,000 per month).

- Employee PF Deduction (12% of Basic): ₹3,600 per month.

- Employer PF Contribution: ₹3,600 per month.

- Under the 2026 Code on Wages Structure:

- Basic Pay (forced to 50%): ₹6,00,000 per year (₹50,000 per month).

- Employee PF Deduction (12% of Basic): ₹6,000 per month.

- Employer PF Contribution: ₹6,000 per month.

The Impact: Your monthly PF deduction has nearly doubled from ₹3,600 to ₹6,000. While your CTC remains exactly the same at ₹12 Lakhs, your monthly take-home cash immediately shrinks because a larger chunk is being forcefully routed into your provident fund account. While younger millennials and Gen-Z employees might lament the loss of immediate liquidity, wealth managers and CAs uniformly agree that the compounding effect of these increased PF contributions will result in massive retirement wealth creation over a 20-to-30-year career horizon.

The Gratuity Revolution and Full & Final Settlements

Gratuity is a statutory benefit paid by an employer to an employee in gratitude for continuous service. Historically, this has been one of the most contentious aspects of Indian labor law, primarily due to stringent eligibility criteria and delayed payouts. The 2026 wage codes completely overhaul this framework.

- Massive Increase in Gratuity Payouts: Gratuity is calculated as 15 days of last drawn Basic Salary for every completed year of service. Because the new wage code forces Basic Salary to be at least 50% of the CTC, the base upon which gratuity is calculated will expand significantly. When you resign or retire, your gratuity payout will be substantially larger than it would have been under older salary structures.

- Reduced Eligibility for Fixed-Term Employees: Historically, an employee had to complete 5 continuous years of service in a single organization to be eligible for gratuity. Recognizing the gig economy and the modern reality of frequent job-hopping, the new wage code reduces gratuity eligibility from 5 years to just 1 year for certain fixed-term and contract employees. This ensures that even short-term workers receive their rightful social security benefits.

- The 2-Day Full and Final (F&F) Settlement Rule: The days of employers holding your final paycheck hostage for 45 to 90 days are over. The new labor code mandates that full and final settlements must be paid within 2 working days of an employee’s exit—whether that exit is via resignation, dismissal, or retrenchment. This is a monumental victory for employee cash flow and financial security during career transitions.

Navigating the Income Tax Act 2025 (Effective April 2026)

The Indian taxation system is witnessing its most significant overhaul in more than six decades. Explicitly stated, effective April 1, 2026, India transitions to the Income Tax Act 2025, completely replacing the legacy Income Tax Act of 1961. The 1961 Act, while foundational, had become bloated with hundreds of complex amendments, provisos, and obscure exemptions. The new Income Tax Act 2025 is designed to be leaner, aggressively promoting the “New Tax Regime” while simplifying tax administration.

The primary goal of the 2025 Act is to push Indian taxpayers away from the deduction-heavy investment strategies (like locking up funds in ELSS or traditional life insurance purely for tax savings) and toward a simplified, flat-rate structure that puts more disposable income in their hands upfront—assuming their PF deductions have not already claimed it.

The FY 2025-26 (AY 2026-27) Tax Slabs

Under the Income Tax Act 2025, the default tax regime offers incredibly lucrative slabs for the middle class. Here is the clear, updated slab structure for the upcoming financial year:

| Income Bracket (₹) | Income Tax Rate |

| ₹0 to ₹4,00,000 | Nil |

| ₹4,00,001 to ₹8,00,000 | 5% |

| ₹8,00,001 to ₹12,00,000 | 10% |

| ₹12,00,001 to ₹16,00,000 | 15% |

| ₹16,00,001 to ₹20,00,000 | 20% |

| ₹20,00,001 to ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Note: Surcharge and Health & Education Cess (4%) apply over and above the calculated tax.

The ₹12 Lakh “Zero Tax” Phenomenon

One of the most attractive features of the new tax laws is the aggressively expanded rebate under Section 87A. Under the Income Tax Act 2025 framework, income up to ₹12 Lakh often results in absolute zero tax liability. How is this mathematical magic achieved?

If your gross taxable income is exactly ₹12,00,000, you first claim the standard deduction of ₹75,000 (which has been enhanced for the new regime). This brings your net taxable income down to ₹11,25,000.

Because your net taxable income is below the newly established rebate threshold, the government grants a full tax rebate on the calculated tax amount. You effectively pay ₹0 in income tax, without needing to submit a single rent receipt or investment proof. This is a massive administrative relief for HR departments and a huge win for junior-to-mid-level employees.

Old Regime vs. New Regime in 2026: Which is Better?

Even with the introduction of the Income Tax Act 2025, the government has allowed the Old Tax Regime to run concurrently for a transitional period, primarily to protect individuals who have made long-term financial commitments (like 20-year home loans). The eternal question remains: Which regime should you choose in 2026?

The Case for the New Regime

The New Tax Regime is the default and is overwhelmingly beneficial for about 75% to 80% of the salaried workforce. You should stick with the New Regime if:

- Your total earnings are near or below ₹12 Lakhs.

- You live with your parents or own a home without a loan, meaning you cannot claim a hefty House Rent Allowance (HRA) exemption.

- You prefer liquidity over locking your money into 5-year fixed deposits, PPF, or Unit Linked Insurance Plans (ULIPs) just to satisfy Section 80C requirements.

- You want a hassle-free tax filing experience without the headache of collecting and verifying investment proofs for your payroll department in January.

The Case for the Old Regime

The Old Regime, while featuring higher nominal tax rates at lower income brackets, allows you to claim powerful deductions under Chapter VI-A. You should actively opt for the Old Regime if you fall into the “Heavy Investment & High Rent” category:

- You pay exorbitant rent in a Tier-1 Metro city (Mumbai, Delhi, Bengaluru) and can claim maximum HRA under Section 10(13A).

- You fully exhaust your ₹1,50,000 limit under Section 80C (EPF, LIC, PPF, tuition fees).

- You invest an additional ₹50,000 in the National Pension System (NPS) under Section 80CCD(1B).

- You are paying high interest on a home loan, claiming up to ₹2,00,000 under Section 24(b).

- You have high premium outflows for health insurance for yourself and senior citizen parents under Section 80D.

The Breakeven Analysis: As a rule of thumb for 2026, if your gross salary is ₹15,00,000, you need to be claiming at least ₹4,25,000 in combined deductions (Standard Deduction + 80C + 80D + HRA + Home Loan Interest) for the Old Regime to mathematically beat the New Regime’s low flat rates. If your total deductions fall below that breakeven threshold, the New Regime will yield a higher in-hand salary.

Example Calculation: The Anatomy of a ₹12 Lakh CTC in 2026

To truly understand how the 50% Basic Pay rule and the Income Tax Act 2025 intersect, let us walk through a highly precise mathematical breakdown of a professional earning a ₹12,00,000 CTC in a metropolitan city.

Assumptions for this Calculation:

- Total Cost to Company (CTC): ₹12,00,000 / year (₹1,00,000 / month).

- Tax Framework: New Regime (Income Tax Act 2025).

- PF Calculation: Both Employer and Employee contributing exactly 12% of Basic Pay.

Step 1: Restructuring to meet the 50% Mandate

To comply with the 2026 Code on Wages, the HR department must set the Basic Pay at a minimum of 50% of the gross.

- Basic Pay: ₹6,00,000 per year (₹50,000 / month).

- HRA (50% of Basic for Metro): ₹3,00,000 per year (₹25,000 / month).

Step 2: Calculating Statutory Employer Costs

The CTC includes the employer’s cost of keeping you on the payroll.

- Employer PF Contribution (12% of Basic): ₹72,000 per year (₹6,000 / month).

- Employer Gratuity Accrual (Approx. 4.81% of Basic): ₹28,860 per year (₹2,405 / month).

Total Employer Deductions from CTC: ₹72,000 + ₹28,860 = ₹100,860.

Step 3: Determining Gross Salary and Flexible Allowances

Your Gross Salary is your CTC minus the employer’s statutory contributions.

- Gross Salary: ₹12,00,000 – ₹100,860 = ₹10,99,140.

- Calculating Remaining Allowances: Gross Salary (₹10,99,140) – Basic (₹6,00,000) – HRA (₹3,00,000) = ₹1,99,140 (This forms your Special Allowance, LTA, etc.).

Step 4: Employee Deductions

Now we calculate what is deducted from your Gross Salary to arrive at your net cash.

- Employee PF Deduction (12% of Basic): ₹72,000 per year (₹6,000 / month).

- Professional Tax (State dependent, assuming max): ₹2,500 per year.

Step 5: Income Tax Calculation (New Regime 2025)

- Gross Taxable Income: ₹10,99,140.

- Less Standard Deduction: ₹75,000.

- Net Taxable Income: ₹10,24,140.

- Tax Liability: Because the Net Taxable Income is well below the ₹12 Lakh threshold under the new 2025 tax slabs, the individual receives a full rebate.

- Total Income Tax Payable: ₹0.

Step 6: Final Take-Home Salary

- Annual Take-Home: Gross Salary (₹10,99,140) – Employee PF (₹72,000) – Professional Tax (₹2,500) – Income Tax (₹0) = ₹10,24,640.

- Monthly In-Hand Cash: ₹10,24,640 / 12 = ₹85,386.

Summary Insight: Out of a ₹1 Lakh monthly CTC, this employee takes home ₹85,386 entirely tax-free, while simultaneously building a robust PF retirement corpus of ₹12,000 per month (combined employee + employer contributions).

FAQ Section: Expert Answers to Your 2026 Payroll Questions

As HR departments scramble to issue updated annexures and employees stare in confusion at their revised payslips, panic is inevitable. As a payroll consultant, I monitor the most common queries and anxieties traversing corporate India. Here are precise, definitive answers to the most frequently searched voice and text queries regarding the 2026 tax and salary changes.

Will my take-home salary decrease in 2026 due to the new wage code?

Yes, for the majority of the corporate workforce, your immediate monthly take-home salary will likely see a slight decrease. If your current employer was structuring your CTC with a very low Basic Pay (e.g., 20% or 30%), the forced recalibration to 50% Basic Pay will significantly increase your Provident Fund (PF) deductions. Since PF is deducted from your gross pay, higher basic equals higher PF, leaving less liquid cash in your hand. However, it is vital to remember that this “lost” money is not gone—it is securely deposited into your PF account, earning sovereign-backed, tax-free interest, vastly accelerating your long-term wealth creation.

Is the new tax regime mandatory for FY 2026-27 under the Income Tax Act 2025?

No, it is not strictly mandatory, but it is the default.

When you submit your investment declarations to your HR department at the start of FY 2025-26, the payroll software will automatically default you to the New Tax Regime. If you wish to claim Section 80C, 80D, or HRA benefits under the Old Regime, you must explicitly inform your employer and select the Old Regime. It is important to note that individuals with business income have restricted flexibility in switching back and forth between regimes compared to purely salaried professionals.How is gratuity calculated under the new 2026 wage code?

The fundamental formula remains similar: (15 / 26) × Last Drawn Basic Salary × Number of Completed Years of Service.

However, the impact is entirely different. Because the Code on Wages mandates that the Basic Salary must be at least 50% of your gross compensation, the multiplier base is now much larger. Consequently, the gratuity lump sum you receive upon leaving an organization will be noticeably higher than it was under legacy payroll structures.Does the 1-year gratuity rule apply to regular full-time employees?

No. The revolutionary drop in gratuity eligibility from 5 continuous years to just 1 year is specifically designed for fixed-term employment (contract workers hired for a specific duration). Regular, permanent employees on indefinite contracts still need to complete the standard 5-year continuous service period to be eligible for gratuity payouts under the current interpretations of the code.

What happens if my employer does not pay my Full and Final (F&F) settlement within 2 working days?

Under the stringent new labor codes, failure to disburse the F&F settlement within the mandated 2 working days after an employee’s exit opens the employer to severe regulatory penalties. If your HR or finance department delays your payout beyond this period, you have the legal right to report the non-compliance to the jurisdictional labor commissioner. In many cases, employers may be liable to pay penal interest on the delayed settlement amount.

I am a freelancer/contractor. Does the 50% Basic Rule apply to me?

No. The Code on Wages and the 50% Basic Pay mandate explicitly govern the “Employer-Employee” relationship. If you are operating as an independent contractor, freelancer, or consultant raising professional invoices (often subjected to TDS under Section 194J), you do not have a standard “CTC” or “Basic Pay.” Therefore, statutory deductions like PF and Gratuity, and the rules governing their restructuring, do not apply to your professional fee income.

If I choose the New Tax Regime in 2026, can I still claim the Standard Deduction?

Absolutely. One of the greatest misconceptions is that the New Regime strips away every single deduction. Under the Income Tax Act 2025, salaried employees and pensioners are legally entitled to a flat Standard Deduction (which has been generously increased to ₹75,000 for the upcoming fiscal). This amount is directly subtracted from your gross salary before any tax slabs are applied, making the New Regime even more financially viable for the middle class.

Moving Forward in 2026

The convergence of the 50% Basic Pay mandate, the 2-day F&F settlement rule, and the comprehensive Income Tax Act 2025 represents the most aggressive pro-employee regulatory modernization in India’s history. While the short-term adjustment phase may cause temporary confusion and minor liquidity crunches due to heightened PF contributions, the systemic outcome is undeniably positive: greater transparency, vastly superior retirement security, and a radically simplified taxation process.

Do not wait for your HR department to spring a surprise annexure on you in April. Use the 2026 Salary Calculator above to simulate your exact tax liability and in-hand cash flow today.